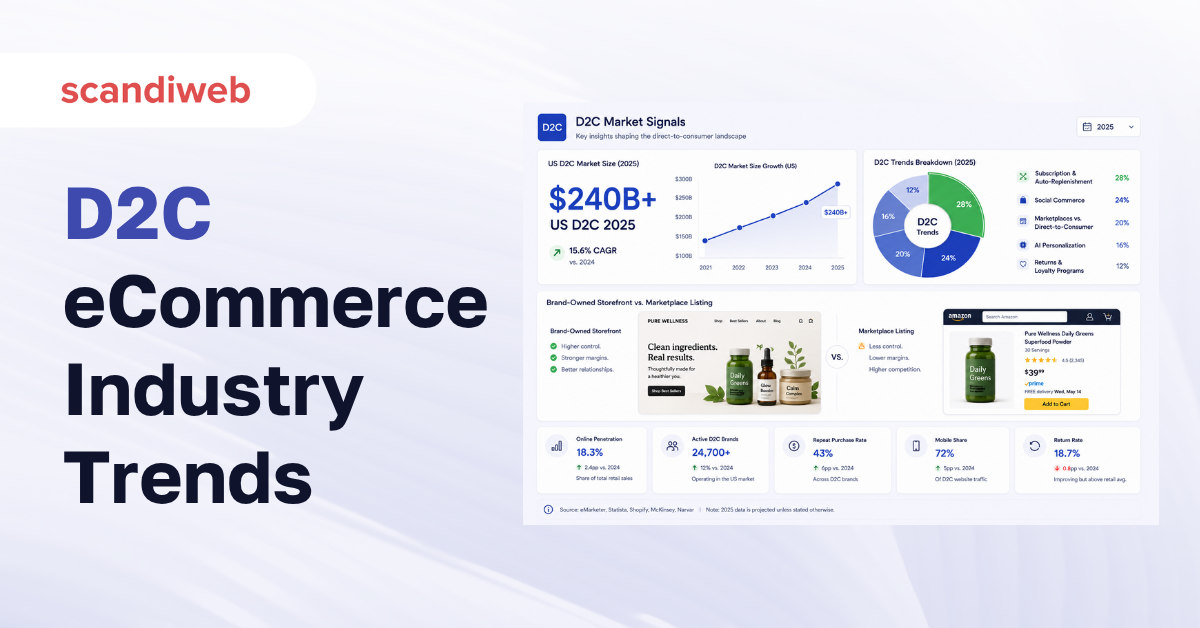

US direct-to-consumer eCommerce reached $239.75 billion in 2025 and now accounts for 19.2% of all US retail eCommerce sales, per eMarketer. That is the number every D2C brand owner should be planning against in 2026. The category has plateaued just under the 20% mark, and the next wave of growth is being decided right now, by which brands pick the right trends to invest in.

This guide is for D2C brand owners and eCommerce marketers who need a clear read on the 2026 picture: what the market actually looks like, the five trends that are moving spend in this cycle, the challenges most likely to stall a D2C brand, and the operating moves that separate the brands compounding from the ones flatlining.

Overview

- US D2C eCommerce is a $239.75 billion category in 2025 at 19.2% share of online retail (eMarketer), globally the market is projected at $595 billion by 2033 (SAP Emarsys).

- The five trends shaping 2026 are AI-driven personalization, omnichannel and social commerce, subscription and loyalty, marketplaces alongside direct, and community-led referral growth.

- Retention, return rates, and customer acquisition cost are the three drag factors most D2C brands underestimate – 2025 returns ran at 19.3% of orders (Shopify), and CAC keeps climbing.

🚀 Quick takeaway

D2C is not slowing – it is maturing. Plateauing share means the easy wins are gone, the next leg of growth depends on the brands that get personalization, omnichannel, and retention working together.

D2C eCommerce market size in 2026

The 2026 baseline is set by three numbers. US D2C sales reached $239.75 billion in 2025 at 19.2% share of US eCommerce (eMarketer). Globally, SAP Emarsys puts the D2C market on a path from $162.91 billion to $595.19 billion by 2033, a roughly 3.5x expansion. BrainSpate puts the global CAGR at 17% through 2033 and pegs the long-run market at $2.7 trillion.

What those numbers really say is that the US market is consolidating and the global market is still expanding. The brands compounding fastest are the ones treating D2C as a channel inside an omnichannel mix, not as a stand-alone storefront. That is also why the share of US eCommerce stopped climbing past 20% – marketplaces and physical retail are still part of the journey for most shoppers.

For an operator, the planning conclusion is straightforward: stop forecasting D2C in isolation. Forecast it against your wholesale, marketplace, and retail channels, and decide where each channel earns its share of the customer.

How big is the D2C eCommerce market in 2026?

The US D2C eCommerce market is about $239.75 billion in 2025, or 19.2% of US eCommerce (eMarketer), and SAP Emarsys projects the global market on a path to $595.19 billion by 2033 from a $162.91 billion baseline. That is a category still growing in absolute dollars, even as its share of US eCommerce flattens.

🚀 Quick takeaway

Globally, D2C is expanding fast. In the US, it is maturing. Both pictures are true at the same time – your investment thesis should reflect which one applies to your brand.

Top 5 D2C eCommerce trends for 2026

Five trends are absorbing the majority of D2C spend in 2026. None of them is new, but the way they combine has changed.

1. AI-driven personalization and discovery. The biggest practical shift is AI moving from “product recommendations” to product discovery. eMarketer flags AI-powered shopping discovery as the new growth driver in 2026, and BrainSpate cites Juniper Research’s $11 billion annual business cost savings tied to AI chatbots. For D2C brands the implication is direct – personalization is now expected on PDPs, search, navigation, and email, not optional in any of them.

2. Omnichannel and social commerce. StoreHippo’s 2026 outlook describes single-channel D2C as no longer competitive: shoppers now move across chat, messaging apps, AI agents, and physical touchpoints inside one buying journey. Social commerce on Instagram and TikTok feeds the top of that funnel, and live shopping is the discovery layer that replaces the static category page for high-consideration categories. The brands winning here treat every touchpoint as part of one journey, not as separate campaigns.

3. Subscription and loyalty. Subscription revenue keeps compounding in consumables (beauty, nutrition, pet, coffee) and the loyalty layer that sits underneath it has become the retention engine. Shopify Enterprise data shows that on its platform D2C first-time orders grew 33% and returning shoppers grew 59% over a two-year window – returning shoppers are now the larger flywheel for most maturing D2C brands. A well-structured eCommerce loyalty program is the operational answer to that math.

4. Marketplaces alongside direct, not instead of direct. Marketplaces (Amazon, TikTok Shop, Walmart) used to be the cannibalization risk D2C brands debated whether to take. In 2026 the working pattern is hybrid: marketplaces feed discovery and reach, the direct store captures the second purchase, the third, the subscription, and the loyalty data. The argument is no longer marketplaces vs. direct – it is which products belong on which channel.

5. Community-led growth and referrals. The strongest first-party number on the table comes from Huel: referral-driven new customer share grew from 10% to nearly 20%, with 22% of customers actively referring (SAP Emarsys, 2025). Community programs, referral mechanics, and brand-led content are now doing the work paid acquisition used to do alone. The brands that build a sharable identity get the math to work, the ones that rely on paid social to compound do not.

🚀 Quick takeaway

Single trends do not move a D2C brand much. The combination of personalization, omnichannel, subscription, hybrid marketplaces, and community is what is moving market share in 2026.

What drives D2C customers in 2026

The center of gravity in D2C is the customer journey. The brands keeping LTV high in 2026 do three things consistently.

They use first-party data well. Shopify’s enterprise data shows returning shoppers grew 59% over two years on its D2C base – the brands seeing that compounding effect are the ones investing in segmentation, identity resolution, and triggered messaging, not just in paid acquisition. The economics shift dramatically the moment you treat returning revenue as the planning baseline rather than the bonus.

They make the buying experience feel intentional. Payment flexibility, delivery options, easy returns, transparent pricing, and a fast PDP – none of these are differentiators in 2026, they are the cost of competing. A brand that holds customer lifetime value high does it by removing friction every quarter, not by chasing a single conversion lift.

They tell a brand story. Community-driven brands convert referrals into customers in a way paid traffic does not – Huel’s referral share doubling to nearly 20% is the public benchmark. Brand identity is the cheapest customer acquisition lever a D2C brand has, and it is the hardest to build under pressure.

🚀 Quick takeaway

First-party data, frictionless purchase, brand story – the three motivators are the same three the best D2C brands have always invested in. The 2026 difference is that the operational expectations are higher in each one.

Top D2C challenges for 2026 brands

Three drag factors decide whether a D2C brand compounds or stalls in 2026.

Retention and return rates. Shopify reports the average eCommerce return rate at 19.3% in 2025, with US returns running close to $850 billion across retail. Apparel and beauty sit higher. Returns directly hit margin and LTV, and the brands fighting them well treat returns as a CX problem (sizing data, PDP clarity, post-purchase support), not just a logistics one. An eCommerce CX audit is the cheapest way to see where returns are actually being created.

Customer acquisition cost. CAC has been climbing for five straight years across the D2C playing field, and the cost of paid social in particular keeps rising while organic reach on Instagram and TikTok stays narrow. The brands holding CAC down in 2026 are the ones building community, referral, and SEO/AEO at the same time, so paid is the amplifier, not the only engine. Sibling trends are showing the same pattern in B2B eCommerce – paid alone no longer compounds.

User experience and journey gaps. Unoptimized PDPs, slow checkouts, weak search, broken cross-device handoffs – any one of these can erase a quarter of acquired traffic before the buying decision is even made. Bounce, cart abandonment, and zero-result search are the three diagnostics worth running monthly, not annually.

🚀 Quick takeaway

Retention math, CAC math, and journey math each matter on their own. The brands compounding solve all three at once, not one at a time.

How scandiweb builds D2C eCommerce for growth

What we see in our client work mirrors what the data says. The D2C brands that compound are the ones treating commerce as one operating system – platform, data, content, and CX all built to work together.

Sports Group Denmark is the clearest example. After replatforming to Magento (Adobe Commerce) with scandiweb, the brand delivered a 10x D2C revenue increase – the kind of step-change a D2C brand can only get when platform, content, and CX investments compound on the same foundation rather than being patched in sequentially. The takeaway from that project is that the platform decision is rarely the bottleneck on its own – it is what the platform enables across the rest of the stack that delivers the result.

We see the same pattern internationally. The Beauty Works expansion case shows the brand entering a new country every 3 months once growth blockers in its technical stack were cleared – the kind of international cadence a D2C brand cannot run when platform changes still take a quarter. International D2C growth, in our experience, is far more often a platform-and-process problem than a marketing problem.

🚀 Quick takeaway

The D2C brands compounding in 2026 are the ones treating their tech stack and their brand investment as the same project. Sports Group Denmark and Beauty Works are two examples of what that looks like in practice.

How do you plan a D2C eCommerce strategy in 2026?

Start from the three numbers that govern your channel mix: where customers find you, where they convert, and where they come back. In 2026, those three answers are usually different channels – discovery on social, conversion split between marketplaces and direct, retention almost always on direct. A 2026 D2C strategy maps each of those steps to the right platform investment, the right data layer, and the right content program – then funds the gaps. Treat the strategy as a 12-month operating plan, not a brand refresh.

FAQ

What is D2C eCommerce?

D2C (direct-to-consumer) eCommerce is the model where a brand sells directly to its end customers through its own digital store, without going through wholesalers, retailers, or marketplaces. The brand controls product presentation, pricing, customer data, and the post-purchase experience, which is what makes the model compounding over time.

How big is the D2C eCommerce market in 2026?

US D2C eCommerce is about $239.75 billion in 2025, or 19.2% of total US eCommerce (eMarketer). Globally, SAP Emarsys projects the D2C market reaching $595.19 billion by 2033 from a $162.91 billion baseline, at a roughly 17% CAGR (BrainSpate).

What are the top D2C eCommerce trends in 2026?

The five trends absorbing most D2C spend in 2026 are AI-driven personalization and discovery, omnichannel and social commerce, subscription and loyalty, hybrid marketplace plus direct, and community-led referral growth. None of them is new in isolation, but the combination is what is moving market share.

What is the biggest challenge for D2C brands in 2026?

Retention, return rates, and customer acquisition cost are the three drag factors most D2C brands underestimate. Average eCommerce return rates ran at 19.3% in 2025 (Shopify), CAC keeps rising on paid social, and journey gaps in PDP and checkout silently erase a meaningful share of acquired traffic.

Should D2C brands sell on marketplaces too?

In 2026 the working pattern is hybrid – marketplaces feed reach and discovery, the direct store captures the second purchase, the subscription, and the loyalty data. The decision is not marketplaces vs. direct, it is which products and which audiences belong on which channel.

How does AI fit into D2C eCommerce?

AI in 2026 D2C is moving from product recommendations to full product discovery, with AI chatbots already credited with about $11 billion in annual business cost savings (Juniper Research, cited by BrainSpate). For an operator that means personalization on PDPs, onsite search, navigation, and email is now a baseline, not a competitive advantage.

What is a healthy D2C retention rate?

There is no single number, but a useful benchmark is that on Shopify’s enterprise base, returning shopper volumes grew 59% over a two-year window. If your returning shopper base is not growing at least in line with first-time order growth, the model is leaking value somewhere – usually in the post-purchase experience.

Planning the next phase of a D2C brand – the platform choice, the channel mix, the retention layer, the AI rollout? Get a 2026 read on which trend to fund first against your category and stage, and plan your D2C strategy with our eCommerce strategy team.

Share on: